Building A1 DDP - Dubai Silicon Oasis

Industrial Area - 342001 -

Dubai - United Arab Emirates

+971 50 756 2346

SERVICES

COMPANY LINKS

SIGN-UP

For Newsletter

You're sitting on tons of customer data.. but struggling to turn it into action. Or maybe your core banking systems are slowing you down when speed matters most.

Either way, the banking sector is evolving fast, and those not keeping up are falling behind fast. The fact is that now digital transformation is the only path forward.

For reference, financial institutions are projected to invest $419.45 billion by 2034 to meet rising customer expectations, improve operational efficiency, and gain a competitive advantage.

In this article, we’ll explore what digital transformation in banking really means today.

You’ll find real examples, common challenges, and proven ways to rethink banking services using AI, cloud computing, data analytics, and more

The banking sector is under pressure to modernize and fast. Customers expect speed, personalization, and 24/7 access across all digital channels.

Fintechs are moving faster. Regulations are stricter. And legacy systems are holding many financial institutions back.

As a result, banks aren’t just adopting tools. They’re overhauling operations to stay competitive.

Globally, digital transformation in banking is seeing the following numbers:

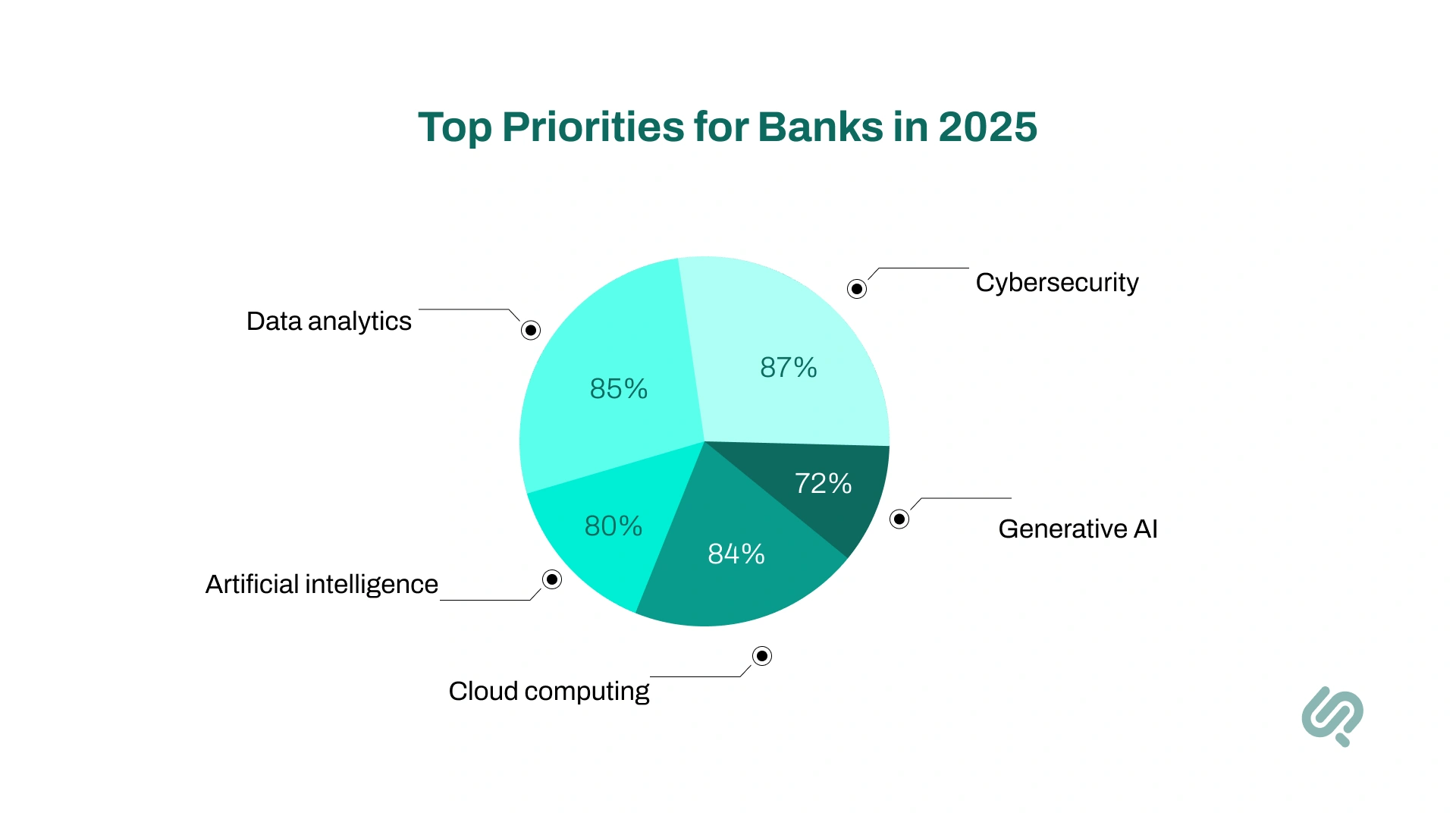

Top areas of investment in 2025 for banks include:

Yet, 70% of digital transformation efforts still fail (8). And while 89% of banks are investing in AI and digital tools, they’re only seeing:

Why? Because tech alone isn’t enough. A successful digital transformation requires strategy, leadership, and alignment. Systems alone won’t cut it.

Behind every successful digital transformation in banking is a stack of powerful tech doing the heavy lifting.

Here are four technologies driving change in the banking industry right now.

AI is reshaping how banks operate at both the front-end and the back-end. In 2025, AI spending in banking is projected to exceed previously forecast numbers of $73 billion.

It's used across the board: powering AI chatbots for e-commerce, detecting fraud in real time, and optimizing risk management.

Where it's helping most:

Generative AI is growing fast too. It's helping banks summarize documents, write code, and support employees with real-time coaching.

This tech is also central to machine learning consultancy and emerging use cases like AI in industrial automation, sports automation, and trading bots.

Cloud computing gives banks the flexibility to scale and innovate without relying on slow, outdated infrastructure. It also supports faster product rollouts and lowers IT costs.

In 2025:

What makes it critical:

Still, the cloud comes with risks (misconfigurations, unclear vendor responsibilities, and the need for strong encryption and MFA). Cloud adoption is powerful, but only when paired with strong planning.

Blockchain has evolved to the point where it’s providing real value in banking operations. Banks use it to speed up cross-border payments, cut costs, and add trust to every transaction.

Highlights:

This tech supports both cost savings and enhanced security, while also enabling innovative financial services that traditional banks struggle to match.

Banks sit on a mountain of customer data, but raw data isn’t enough. The ability to analyze customer data in real time is what sets digital leaders apart.

In 2025, the majoirty of banks are prioritizing advanced data and AI analysis tools.

Used for:

This is the foundation of modern digital banking transformation, from mobile apps to wealth management. Banks that manage data well gain speed, accuracy, and a real competitive advantage.

Banks aren’t transforming in theory. They’re solving real problems, right now. From improving onboarding speed to launching entirely new business models, digital transformation is reshaping how banks operate and serve people.

Here’s how it’s showing up in the real world.

Banks are using artificial intelligence to meet rising expectations for faster, simpler support. This shift is about more than convenience, it’s about relevance.

What’s working:

By combining data sets in machine learning with customer insights, banks now deliver smarter, more helpful interactions at scale.

The back office is getting leaner. Banks are using digital transformation in BPM to streamline tasks, cut costs, and increase speed, without compromising accuracy.

Real-worl results:

Banks using AI and machine learning to automate critical processes are not only cutting overhead. They’re reducing errors and improving compliance.

The way customers conduct transactions has changed. Fast, secure, and mobile-first payments are now standard, not a bonus.

Key developments:

By investing in AI workflow automation and blockchain, banks are offering payment experiences that are quicker, safer, and built around how customers actually live.

As cyber threats evolve, banks are fighting fire with fire, using AI to detect fraud, secure logins, and assess risk in real time.

Where AI helps:

Regardless of the industry, security is a top priority. Having a digital advantage allows you to build trust with customers.

An example of strengthened security through digital transformation can be found here in this AI cloud surveillance platform project we completed for a client.

Some banks are doing more than improving operations. They’re rethinking their entire approach to service delivery.

New directions include:

With support from custom AI model development and machine learning development services, these models allow banks to serve new customer segments, faster, cheaper, and with more flexibility.

For every success story in digital transformation in banking, there are dozens of projects that stall or fail outright. While the technology is improving, the path forward is still full of roadblocks.

Here are five major challenges banks face today.

Many traditional banks still rely on outdated, inflexible core banking systems. These systems are hard to scale, expensive to maintain, and don’t connect well with new digital tools.

Key issues:

Instead of ripping everything out at once, banks need a gradual strategy, replacing components one by one while avoiding a full system shutdown.

Compliance isn’t just a checkbox. It’s a moving target. Banks must keep up with data privacy regulations like GDPR and CCPA, plus industry-specific rules like DORA and SEC requirements.

Challenges include:

For a successful digital transformation, every new feature must pass through a regulatory lens. That takes planning, audits, and clear processes.

As digital services expand, so does the attack surface. Cybercriminals are getting smarter, using deepfake scams, supply chain exploits, and AI-powered attacks to breach systems.

Emerging threats:

Banks need robust security models that adapt fast, are fueled by AI, monitored in real time, and built into every layer of the stack.

The banking industry is racing to adopt digital technologies, but there’s a global shortage of skilled talent to lead and manage these changes.

Top challenges:

Some banks are turning to no-filter AI chatbots or exploring the best AI tools for coding to offset labor gaps. But long-term success requires building internal capability, not just outsourcing it.

Digital projects often overrun budgets or underdeliver. Banks start with big goals but hit roadblocks during execution, especially when measuring real value.

Why ROI is hard to prove:

To move forward, banks need phased execution, better planning, and a clear link between each digital investment and business outcomes.

Banks that embrace digital transformation aren’t just catching up. They’re pulling ahead.

With the right strategy, they’re building smarter operations, deeper customer loyalty, and entirely new ways to grow.

Across the banking industry, digital-first experiences are becoming the norm. Customers expect fast support, simple online transactions, and tools tailored to their needs. Banks that deliver see stronger customer engagement, faster customer acquisition, and greater loyalty.

On the backend, digital tools help reduce costs and increase flexibility.

Cloud, AI, and automation cut waste, break down data silos, and improve decisions through advanced data analysis.

Some of the biggest opportunities ahead include:

The future of banking will be built around rapid response, deeper insights, and stronger connections.

Banks that start now can lead (not follow) the next wave of innovation.

These examples show how leading firms are using digital technologies to solve real problems, meet customer needs, and gain an edge in the evolving banking industry.

JPMorgan Chase has been at the forefront of using AI and cloud technologies to modernize its operations. One of its biggest digital priorities has been fraud detection at scale.

These efforts address key challenges like fraud risk, customer trust, and infrastructure agility (all part of a wider digital transformation process).

Spanish bank BBVA has emerged as one of the most aggressive adopters of generative AI in banking.

By embedding generative AI into operations, BBVA is reshaping how banking teams work and support evolving customer behavior.

HSBC has been pushing the boundaries of blockchain in investment banking and cross-border operations.

These initiatives help HSBC streamline complex processes, reduce costs, and better serve international clients. All while responding to shifts in market trends and regulatory expectations.

PenFed Credit Union partnered with Salesforce to deploy Einstein AI, aiming to improve customer engagement and reduce call center strain.

This shows how even smaller financial institutions can adapt the mobile-first banking experience to match what modern customers expect.

The pace of digital transformation in banking is no longer up for debate, only the approach is.

From AI to blockchain, the tools are ready. The real challenge is aligning them with strategy, customer needs, and execution.

Whether you're modernizing legacy systems or launching new digital services, success comes from moving deliberately, not just fast.

Start small, stay focused, and scale what works.

In a world where customer expectations and risks evolve daily, the banks that lead will be the ones that adapt with clarity and purpose.

1. Digital Transformation in BFSI Market

2. Top Digital Banking Platforms & Competitors

3. Neobanks and the Next Banking Revolution

4. Digital Banking Statistics 2025

5. Digital Transformation Trends and Stats

6.Online and Mobile Banking Statistics

7. Boosting Financial Inclusion in Africa

8. Common Pitfalls in Transformations

Musa is a senior technical content writer with 7+ years of experience turning technical topics into clear, high-performing content.

His articles have helped companies boost website traffic by 3x and increase conversion rates through well-structured, SEO-friendly guides. He specializes in making complex ideas easy to understand and act on.