Building A1 DDP - Dubai Silicon Oasis

Industrial Area - 342001 -

Dubai - United Arab Emirates

+971 50 756 2346

SERVICES

COMPANY LINKS

SIGN-UP

For Newsletter

Every click, payment, and login you make leaves a digital trace, and hackers are always a step behind, waiting to exploit it.

That’s why blockchain security has become the backbone of digital trust.

It doesn’t just store data. It locks it inside cryptographic chains that no single entity can tamper with.

Forget centralized servers that crumble under one breach, blockchain distributes control across thousands of nodes.

Each transaction is verified, encrypted, and permanently recorded, making manipulation virtually impossible.

And the best part? With blockchain security audits, organizations can now spot weaknesses before attackers do.

The result? Faster, safer, and more transparent digital transactions, built for a future where trust is non-negotiable.

Blockchain security is the combination of cryptography, decentralization, and consensus validation that ensures transactions and data remain tamper-proof

Instead of relying on a single database, blockchain distributes data across multiple nodes, making unauthorized changes nearly impossible.

Every transaction is encrypted, verified, and permanently recorded, ensuring trust without intermediaries.

Example:

When two banks exchange funds using blockchain, each transaction is digitally signed and validated by all nodes before being added to the ledger, preventing fraud or double-spending.

Not all blockchains are created equal. The level of security and privacy depends on the type of blockchain and its governance model.

Example:

Banks in the We.Trade consortium use a private blockchain to verify and record trade transactions. This helps eliminate disputes and ensures that every payment is validated securely between members.

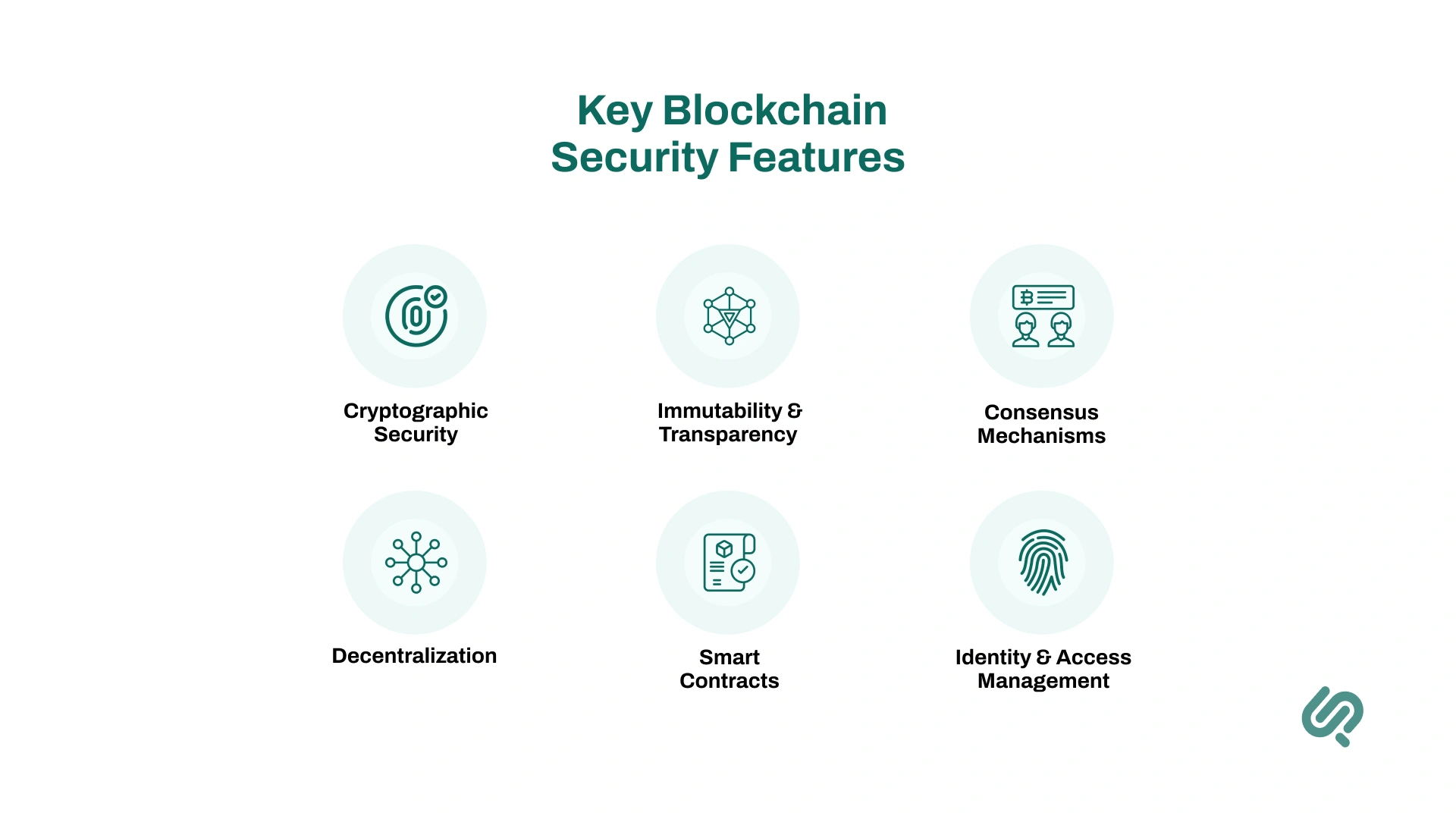

Blockchain’s strength lies in its layered security design.

Below are the core features that make it one of the most reliable technologies for securing digital transactions and sensitive data.

Beyond securing transactions, blockchain also protects sensitive information and user identities.

Its built-in privacy mechanisms, encryption, and controlled data sharing make it a powerful tool for safeguarding digital assets across industries.

One of the strongest advantages of blockchain technology is its ability to guarantee data integrity.

Because blockchain records form an immutable record, any transaction or stored datawhether it’s a financial transaction or medical data, cannot be silently changed once confirmed.

Each block is cryptographically linked to the previous block, making it nearly impossible for attackers to alter information without breaking the entire chain.

This tamper-resistant structure acts as a safeguard against data breaches and ensures that every piece of blockchain data remains trustworthy over time.

Blockchain also improves data protection through controlled sharing.

Instead of storing sensitive information such as identity data or private health records directly on the chain, organizations can keep that data off-chain and store only hashes or pointers in the distributed ledger.

This allows others to verify the data integrity without exposing the raw information. Advanced techniques like zero-knowledge proofs take this further, enabling one party to confirm facts such as age or identity without revealing the underlying details.

This balance of transparency and privacy makes blockchain a secure method for verifying transactions while keeping private data safe.

The rise of digital identity solutions highlights another important application of blockchain.

Instead of relying on centralized databases that are prone to identity theft and hacking, blockchain enables self-sovereign identity on a distributed ledger.

In this model, users maintain control over their credentials, secured cryptographically across multiple nodes.

Large financial institutions are already piloting blockchain-based ID systems to allow individuals to store and share personal information directly from their devices securely.

These solutions not only enhance data privacy but also address real-world challenges such as synthetic identity fraud, which costs banks billions each year. With blockchain, identity data becomes safer, more private, and far less vulnerable to exploitation.

Another key security feature of blockchain lies in access management and encryption.

In permissioned blockchains, only authorized participants with the right access privileges can view or add data, making it highly effective for enterprises managing sensitive information like medical or financial records.

Strong cryptographic techniques and robust key management ensure that even if a network node is compromised, encrypted transaction details remain protected.

Combined with strict membership and access controls, this layered security approach helps businesses maintain compliance with privacy regulations while reinforcing confidence in their blockchain systems.

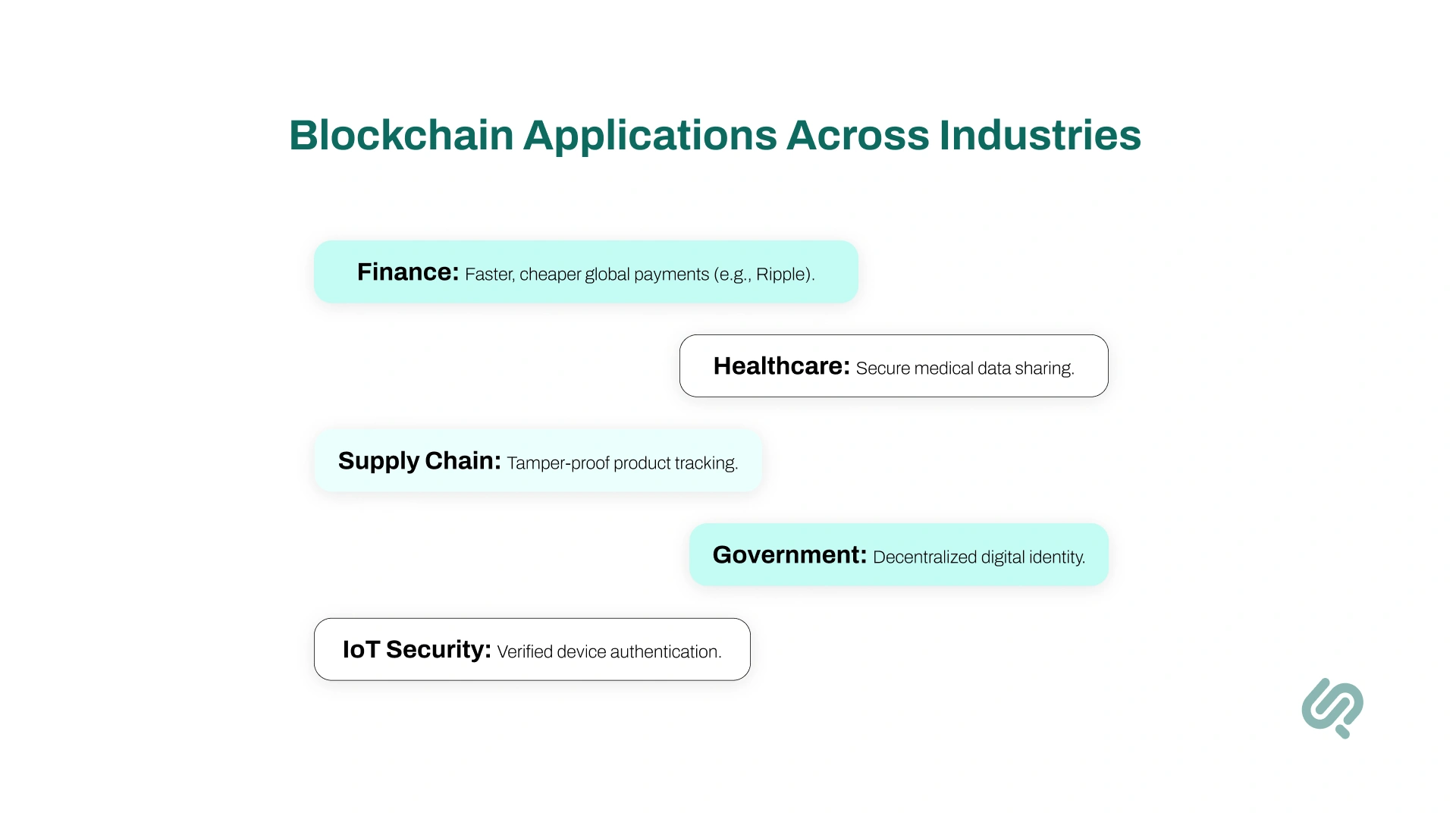

Blockchain’s versatility extends far beyond cryptocurrency.

Its security and transparency are now powering digital transformation across multiple sectors, from finance to healthcare and logistics, wherever trusted, verifiable transactions are critical.

Finance was the first sector to prove the value of blockchain security solutions.

By removing intermediaries, blockchain enables faster, cheaper cross-border transfers and near real-time settlements.

For instance, Ripple allows banks to complete international payments in seconds instead of days.

Beyond cryptocurrencies like the Bitcoin blockchain, major banks are adopting permissioned blockchains for interbank settlements, gaining benefits like fraud protection, immutable records, and secure financial transactions.

With healthcare facing thousands of data breaches every year, blockchain in healthcare offers a secure way to protect medical data.

Records can be encrypted and stored, with patients in control of how they are shared.

Hospitals connected through a distributed ledger can access up-to-date patient histories while preventing unauthorized changes.

For example, blockchain-based systems reduce duplicative testing and improve care while ensuring data integrity and data protection for sensitive health records.

Blockchain’s transparent ledger strengthens supply chain trust by recording every step a product takes from source to shelf.

Luxury brands and food producers now use blockchain in supply chain to verify authenticity and prevent counterfeits.

Because all transaction details are stored on-chain, attackers can’t alter shipment records without alerting the entire network of nodes.

This ensures supply chain integrity, reduces fraud, and provides tamper-proof tracking for goods worldwide.

Governments are turning to blockchain technology for citizen services.

Decentralized IDs and verifiable credentials let people prove attributes like age, citizenship, or vaccination status without storing all identity data in a hackable central database.

During the pandemic, fake vaccine certificates were common, blockchain-based certificates could have ensured authenticity.

Countries such as Italy, the U.S., and Brazil are piloting blockchain digital identity systems, aiming to cut identity theft and enable more secure e-government services.

The growth of IoT creates huge risks, with millions of devices needing secure authentication.

Blockchain in cybersecurity assigns each device a digital identity, verifying that data comes from legitimate sources.

In industrial IoT, blockchain combined with edge computing ensures that transaction data from sensors cannot be spoofed or altered.

This enhances data integrity across connected devices and prevents malicious nodes from injecting false information into blockchain networks.

While blockchain is highly secure by design, it’s not completely immune to challenges. Scalability, integration, and human error can still create weak points if not properly managed. Understanding these vulnerabilities is key to maintaining trust and performance in blockchain systems.

One of the most discussed blockchain security challenges is scalability. Public blockchains such as Bitcoin and Ethereum can process only a limited number of secure transactions per second, causing congestion, slow confirmations, and higher fees during peak times.

This performance bottleneck impacts time-sensitive applications from real-time trade settlements to blockchain in intellectual property, where verifying ownership or licensing rights requires fast and reliable processing.

While Layer-2 solutions and sidechains are improving throughput, scalability remains a key hurdle for the widespread adoption of blockchain security solutions.

Although the blockchain protocol itself is cryptographically strong, vulnerabilities often appear in the surrounding ecosystem.

Phishing attacks and private key theft remain the most common threats to blockchain for business, as stolen keys give attackers direct access to wallets.

Smaller networks can face 51% attacks, where an attacker with majority control of hashing power can rewrite history.

Sybil attacks allow malicious actors to create multiple fake nodes to disrupt consensus, while routing attacks intercept data between network nodes to manipulate traffic. (1)

Additionally, smart contract bugs such as reentrancy or overflow errors have led to major breaches, highlighting the need for continuous testing and secure coding practices.

Adoption also faces regulatory challenges. Immutable blockchain logs often conflict with privacy laws like the “right to be forgotten”, and legacy IT systems are not always compatible with blockchain technology security standards.

Businesses must balance compliance with industry regulations while maintaining the data integrity benefits of decentralized systems.

This complexity makes integration one of the toughest barriers to mainstream blockchain implementation.

Many blockchain security vulnerabilities do not come from the chain itself but from poor implementation. Misconfigured keys, unencrypted data payloads, or weak access controls open the door to breaches.

Research shows that nearly half of crypto hacks exploit known flaws or social engineering rather than fundamental blockchain weaknesses.

This underlines the importance of blockchain security audits and robust governance models before deploying solutions at scale.

Technology alone cannot guarantee security. Human error, weak passwords, mishandled private keys, or falling victim to phishing remains one of the largest risks.

Because blockchain removes centralized intermediaries, users bear full responsibility for access management and disaster recovery.

Best practices include multi-signature wallets, key revocation methods, and strong user education. Without these safeguards, even the most advanced blockchain systems can be compromised.

Finally, proactive blockchain protocol security audits are essential to identify weaknesses before attackers exploit them.

These audits should evaluate consensus mechanisms, smart contracts, APIs, and integration layers, ensuring no hidden loopholes remain.

Today, specialized firms focused on blockchain security improvements in action provide continuous monitoring, vulnerability assessments, and penetration testing to strengthen defenses.

Without such rigorous testing, even the most well-designed blockchain systems can fail under real-world attack conditions.

While blockchain itself is highly secure, attackers often exploit weaknesses in surrounding systems or user behavior.

Common blockchain attack methods include:

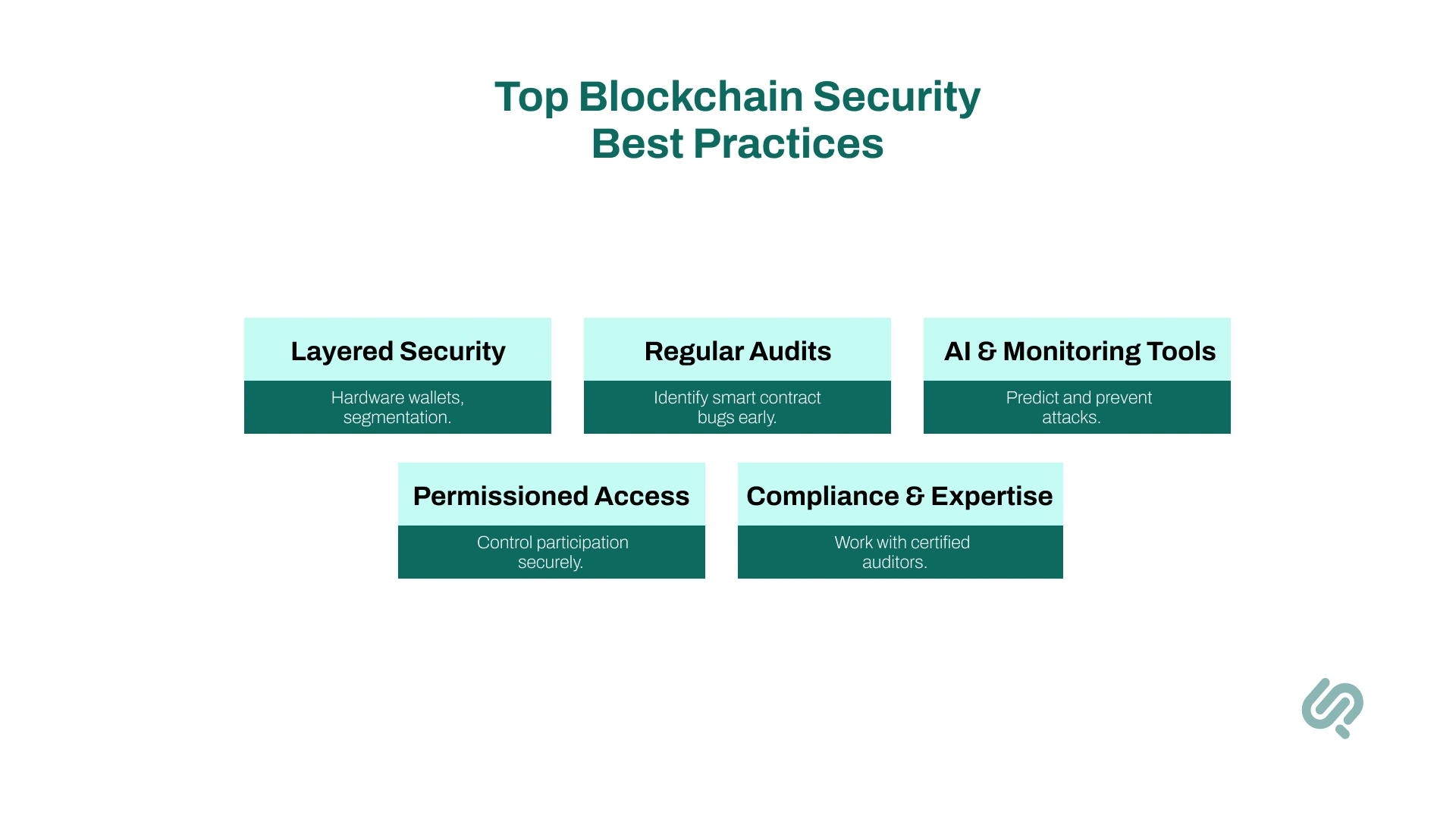

To keep blockchain networks truly secure, organizations must pair blockchain’s built-in cryptography with enterprise-grade security practices.

These blockchain trends, ranging from multi-layer encryption to permissioned access, help prevent breaches, strengthen compliance, and ensure operational resilience.

Modern blockchain systems mix built-in cryptography with enterprise-grade controls.

Hardware wallets and multi-signature approvals protect credentials, while network segmentation ensures that only authorized nodes have access to sensitive data.

Example:

Hyperledger Fabric enforces access through certificate-based identity management, reducing unauthorized entry points.

2. Security Audits and Testing

Before deployment, companies run security and protocol audits to detect bugs in smart contracts or consensus rules.

Automated scanners, manual code reviews, and stress tests help uncover backdoors and vulnerabilities..

Example:

Auditors like CertiK and ConsenSys Diligence help projects avoid million-dollar exploits by testing every contract and transaction path.

New security tools constantly monitor blockchain networks.

Intrusion Detection Systems adapted for blockchain can flag suspicious spikes in activity (like a 51% attack). Smart contract scanners detect issues such as overflow errors or reentrancy bugs.

Example:

Chainalysis and SlowMist provide real-time blockchain threat analytics for banks and exchanges.

Private or consortium blockchains offer stronger control by limiting access to trusted members, ideal for sectors like banking or healthcare.

IBM notes that permissioned systems rely on selective endorsement among known participants, ensuring accountability.

Example:

We Trade, a banking consortium blockchain, uses member-only permissions to prevent fraud in trade finance.

Blockchain complements traditional cybersecurity systems. For instance, companies record hashes of system logs on-chain to detect tampering instantly.

The U.S. Department of Homeland Security found 54% of organizations using blockchain do so to prevent phishing and man-in-the-middle attacks (2).

Example:

Guardtime, an Estonian cybersecurity firm, secures government records with blockchain-based integrity checks.

Because blockchain security is complex, firms rely on specialists like IBM, ConsenSys, and EY for compliance audits, KYC/AML design, and data privacy assurance.

These experts ensure systems meet standards such as GDPR and financial regulations.

Example:

Ernst & Young’s OpsChain helps financial institutions run compliant, secure blockchain transactions.

When implemented correctly, blockchain cuts fraud and boosts transparency. A major banking consortium reported reduced transaction fraud after automating verification via blockchain.

Every access is logged, making unauthorized use immediately visible.

Example:

In the CULedger network’s MemberPass deployment, credit unions reported they could reduce fraud expenses in call centers by up to $150,000 annually by improving identity authentication and reducing fraudulent account access.(3)

Blockchain eliminates centralized ID databases; users instead control their data using digital signatures.

This reduces synthetic identity fraud, which costs banks over $6 billion annually, according to Fortune Business Insights.

Example:

Microsoft’s ION project gives users decentralized IDs, protecting privacy while maintaining verification integrity.

Blockchain security continues to evolve.

Hybrid consensus models (PoW + PoS), quantum-resistant encryption, and AI-powered anomaly detection make networks smarter and safer.

Example:

Clarity Ventures reports that AI-integrated blockchain monitoring can predict attacks before they occur, strengthening long-term defense.

Formal verification mathematically proves that a smart contract will execute exactly as intended, leaving no room for logical flaws or exploits.

It goes beyond traditional testing by analyzing all possible scenarios, ensuring the contract’s logic is error-free and tamper-proof before deployment.

Example:

Projects like Tezos and Runtime Verification use formal methods to safeguard billions in digital assets, achieving the highest level of blockchain code assurance through mathematically verified security.

Let’s look at what the future of blockchain security looks like:

Blockchain is transforming digital security by providing a decentralized, tamper-proof way to record and verify transactions.

Its cryptographic protection, smart contracts, and decentralized structure eliminate single points of failure and reduce the risk of data breaches.

From finance to healthcare, blockchain ensures secure data exchange, builds trust, and enhances privacy.

As adoption expands, it will continue to redefine how organizations protect digital assets and conduct secure transactions in the connected world.

Ameena is a content writer with a background in International Relations, blending academic insight with SEO-driven writing experience. She has written extensively in the academic space and contributed blog content for various platforms.

Her interests lie in human rights, conflict resolution, and emerging technologies in global policy. Outside of work, she enjoys reading fiction, exploring AI as a hobby, and learning how digital systems shape society.