Building A1 DDP - Dubai Silicon Oasis

Industrial Area - 342001 -

Dubai - United Arab Emirates

+971 50 756 2346

SERVICES

COMPANY LINKS

SIGN-UP

For Newsletter

Blockchain is a secure, distributed ledger technology that’s reshaping how companies run their business operations.

In simple words, it’s a shared record of transactions that everyone in the network can see and trust. Each new entry becomes part of an immutable (unchangeable) chain of blocks.

No single party controls blockchain for business, so all the stakeholders, partners, suppliers, and auditors work from the same real-time data.

As blockchain eliminates unnecessary middlemen, it introduces transparency, trust, and operational efficiency to workflows that were previously slow.

Analysts estimate that widespread adoption could add $1.76 trillion to global GDP by 2030, proof that this cutting-edge technology is more than hype for modern business operations (1).

Blockchain for business is the use of distributed ledger technology to securely record and share transactions, giving all stakeholders access to the same real-time, tamper-proof data.

Businesses value blockchain because it builds trust and enhances security.

Furthermore, it streamlines operations through transparent, tamper-proof, and efficient digital transactions.

A few standout elements of blockchain include:

Blockchain boosts efficiency and cuts costs by automating processes, eliminating intermediaries, and enabling real-time peer-to-peer transactions that reduce manual work and transaction fees.

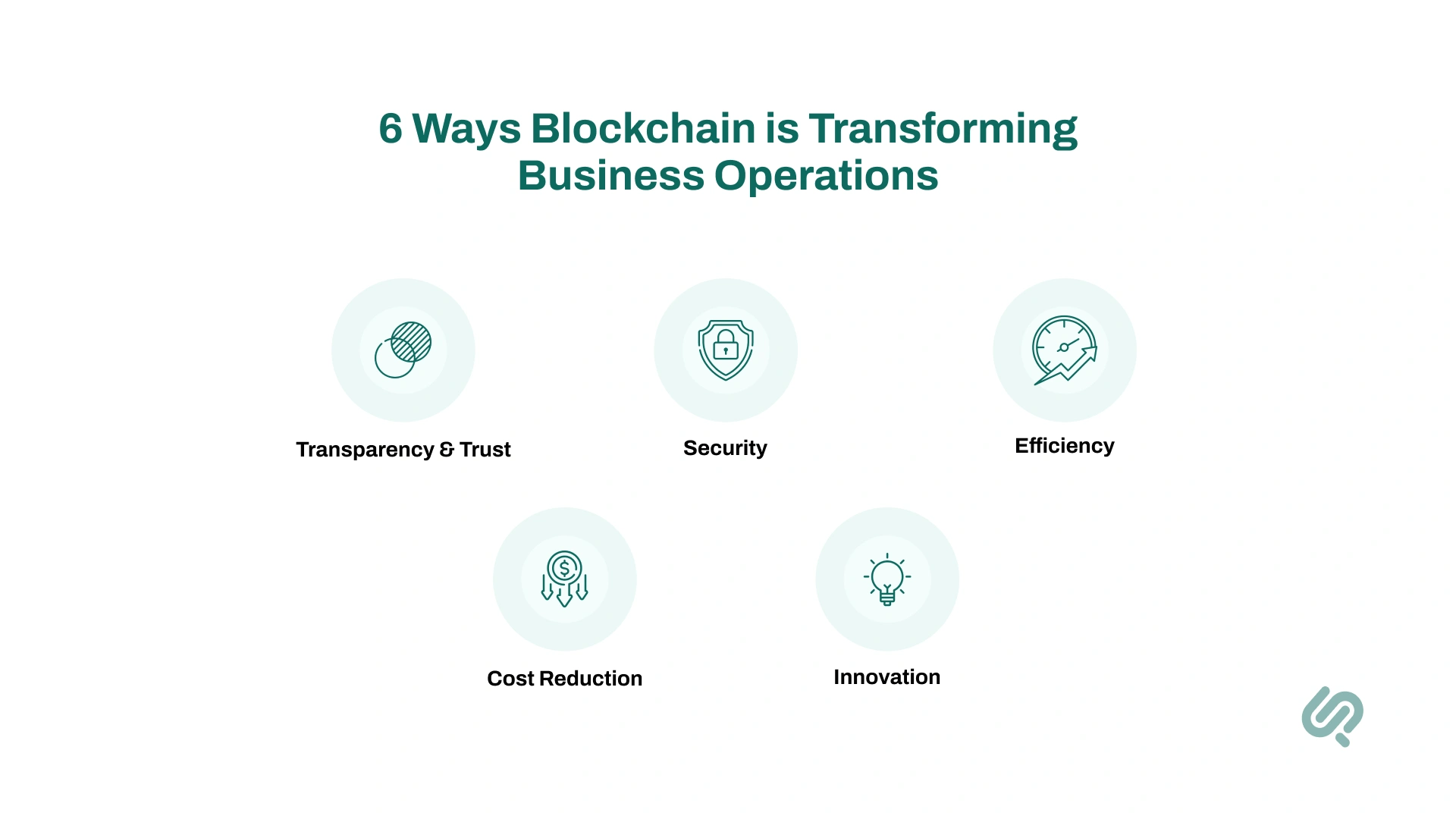

Blockchain is steadily becoming a core part of how companies operate.

It strengthens trust, improves security, and helps businesses run more efficiently. Below are the main ways it is reshaping modern business operations:

Blockchain’s distributed ledger technology ensures that every transaction is visible to authorized participants. This creates a single source of truth that all partners, suppliers, and auditors can rely on.

Each block is securely linked to the one before it, making unauthorized changes nearly impossible without network approval. This cryptographic structure strengthens data security and reduces risks.

Through smart contracts, blockchain automates tasks that normally require manual oversight. These digital agreements execute instantly when predefined conditions are met.

Blockchain helps organizations significantly reduce costs by cutting out middlemen and duplicate record-keeping.

Beyond efficiency, blockchain is enabling innovative solutions and fresh approaches to value creation.

Supply chains are complex and vulnerable to disruption. Blockchain provides supply chain transparency and traceability that builds resilience.

Blockchain is no longer just a back-end technology. It is actively reshaping how businesses function day to day.

From automating agreements to securing data, its impact is visible across critical operations.

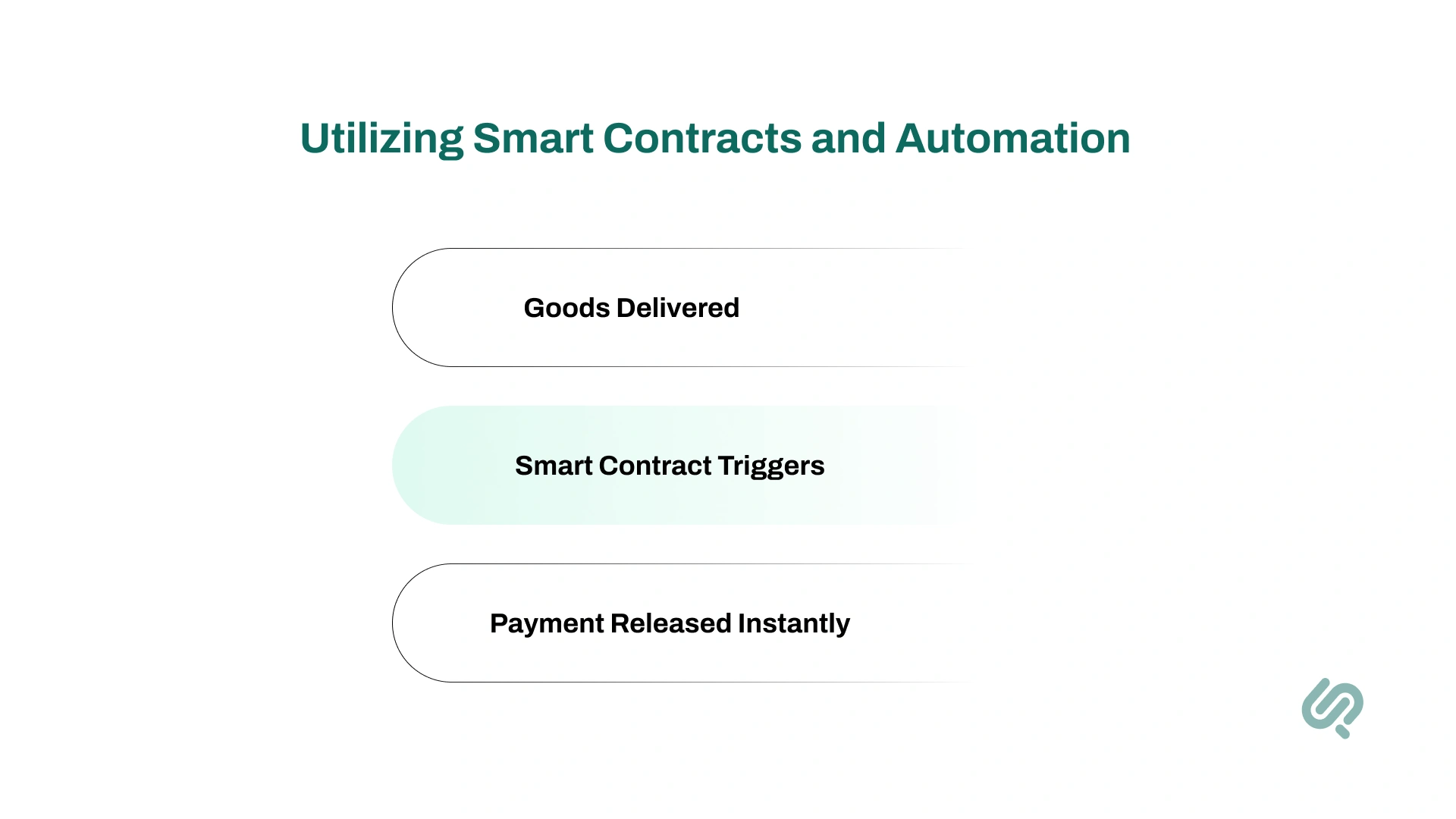

One of blockchain’s most powerful features is the smart contract. These are pieces of code stored on the blockchain that automatically carry out actions when certain conditions are met.

For example, once goods are delivered, a smart contract can instantly release payment. No paperwork or waiting for manual approval.

This automation reduces human mistakes, speeds up transactions, and creates operational efficiency.

In industries like logistics or insurance, smart contracts streamline claims, customs clearances, and shipment handoffs, removing the need for middlemen and reducing delays.

Beyond individual contracts, companies are adopting decentralized applications (dApps) that run on shared ledgers. These dApps manage tasks like supply chain tracking, customer reward programs, and inter-company settlements.

By encoding business logic directly into the blockchain, enterprises essentially build tamper-proof digital rules that execute themselves, leaving businesses free to focus on growth instead of paperwork.

The impact of blockchain is obvious in supply chain management.

Complex global supply chains face issues like poor visibility, counterfeit goods, and sudden disruptions. Blockchain addresses these problems with end-to-end traceability and resilience.

This reduces disputes, eliminates lost paperwork, and builds supply chain transparency.

For example, IBM and Maersk’s TradeLens platform has tracked over 30 million shipments, proving blockchain’s scalability in logistics. Nestlé and UPS have also piloted blockchain for early delay detection, boosting supply chain resilience.

Market outlook: According to a report by Grand View Research, the global blockchain supply chain market was valued at USD 2,258.1 million in 2023 and is projected to grow to USD 192,927.7 million by 2030, with a CAGR of 88.8% from 2024-2030 (3)

Some forecasts put blockchain supply chain spending even higher, at over $3 trillion by 2026. These figures underline the importance of trusted tracking in the digital age.

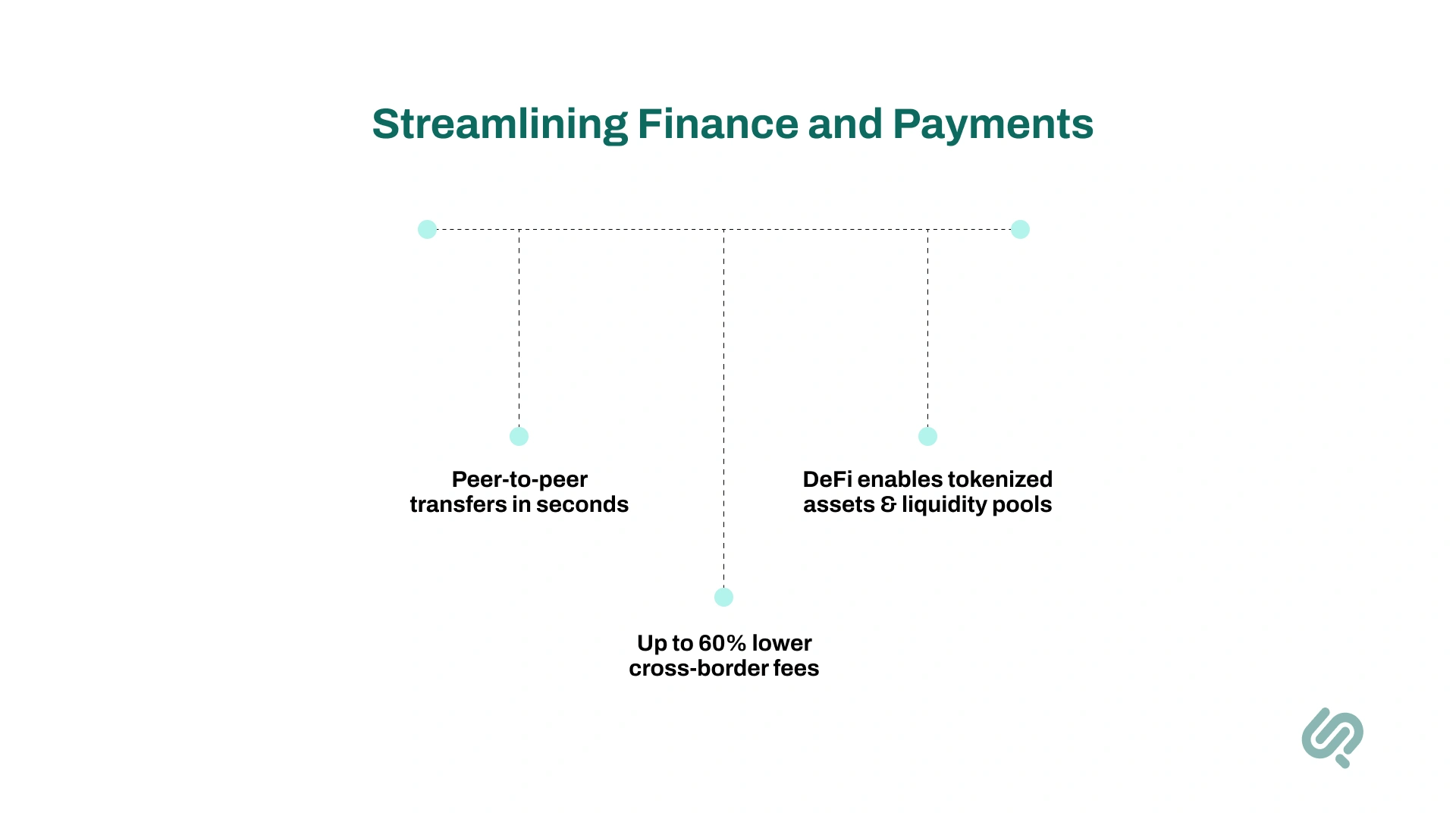

Traditional financial systems are slow and costly, particularly for cross-border payments. Transfers often take days and involve multiple intermediaries, each adding fees. Blockchain changes this by allowing peer-to-peer transfers that settle in seconds at a fraction of the cost.

Smart contracts enhance this even further. Invoices, loans, and securities can be issued on-chain and settle automatically when conditions are met. Compliance rules embedded in code reduce errors and speed up audits.

Blockchain is also paving the way for decentralized finance (DeFi) in enterprises. Businesses can tokenize assets, manage liquidity through decentralized pools, or even experiment with crypto-payroll with greater transparency and lower friction than legacy systems.

Example: In cross-border payments, blockchain can reduce settlement times from days to seconds, while significantly lowering fees.

Loyalty programs are also evolving. Companies now use blockchain to create interoperable reward points, making customer engagement seamless.

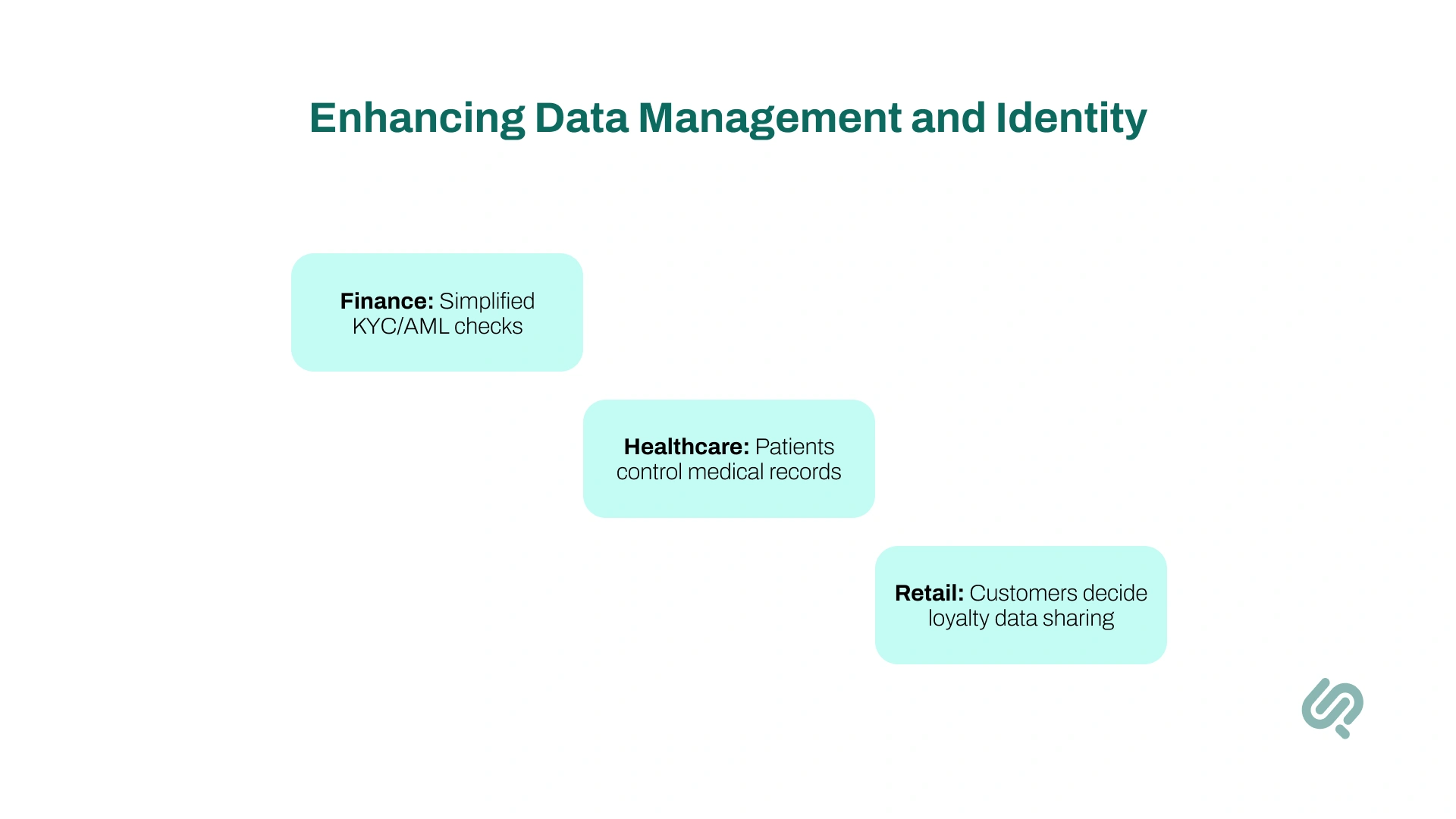

Beyond finance and supply chains, blockchain is transforming how organizations manage data and identities.

Businesses today handle highly sensitive information. Customer details, contracts, financial flow records, and even medical records often need to be shared across multiple parties.

Traditionally, this created risks: siloed systems, duplication, and exposure to breaches.

Blockchain offers a new model by providing a secure, distributed ledger where data can be validated without revealing its raw content.

Instead of storing personal data directly, companies can keep data hashes on the blockchain. These hashes prove the integrity of information while leaving the actual data stored off-chain in secure databases.

This ensures privacy while guaranteeing that any tampering is instantly detectable. Governments are already showing the way. Estonia, for example, has created a nationwide blockchain-secured digital identity system that covers more than 98% of its citizens. (4)

A key innovation here is a self-sovereign identity blockchain-based identity framework that allows people to control their own information.

Instead of sharing entire documents, individuals can provide only the data that’s required. For example:

Across these sectors, blockchain ensures that once information is recorded on the blockchain network, it is immutable, tamper-proof, and visible to all the stakeholders who need access.

This not only eliminates duplication and unnecessary manual checks but also fosters trust in digital interactions, something essential as enterprises enter the digital age.

Blockchain has moved far beyond crypto and is now shaping modern business operations across industries.

From supply chain management to finance and aviation, enterprises are using blockchain to build trust, improve efficiency, and create new business models.

Blockchain in healthcare ensures medical records remain secure and verifiable while allowing patients to control access.

Pharmaceutical companies also use it to track drugs from production to pharmacy shelves, reducing counterfeit risks and improving patient safety.

A World Economic Forum initiative, IBM Food Trust, is already deployed in food distribution. It enables retailers to trace produce origins instantly.

What once took days, like tracking a shipment of mangoes, can now be done in seconds, improving both safety and supply chain transparency.

Global logistics players such as UPS integrate blockchain with IoT sensors to monitor freight in real time.

This reduces risks like spoilage or tampering and strengthens supply chain resilience, ensuring more reliable deliveries across global supply chains.

Luxury brands are using blockchain to guarantee authenticity. Alibaba’s certified supply chain program, for example, helps verify the origin of high-end goods.

This protects customers from counterfeits while building trust in digital-first retail environments.

Even airlines are experimenting with blockchain.

British Airways has tested blockchain for tracking aircraft parts and improving passenger data management, creating operational efficiency in an industry where safety and reliability are non-negotiable.

The financial sector leads in blockchain adoption. Banks and insurers worldwide, including JPMorgan and HSBC, run blockchain pilots for trade finance and settlement systems.

Platforms like Ethereum and Hyperledger are being used by companies such as Adobe and Allianz for digital contracts, business processes, and compliance.

This makes finance the sector with the strongest blockchain adoption to date

Blockchain is now a network of trust underpinning new business models.

Across industries, it enables solutions like decentralized supply chain platforms, cross-border payments, digital identity frameworks, and on-chain marketplaces.

These use cases show how blockchain is truly transforming business operations across multiple sectors in the digital age.

While blockchain holds immense potential for transforming modern business operations, adoption is not without obstacles.

Companies must weigh technical, financial, and organizational hurdles before rolling out blockchain solutions for business at scale.

One of the most cited challenges is scalability. Many blockchain networks process fewer transactions per second than legacy payment systems, creating delays for industries with high-volume operations.

The cost of implementation is another concern. Setting up infrastructure, training staff, and hiring blockchain development services can strain budgets, especially for medium-sized enterprises.

Businesses also face uncertainty around regulations, particularly concerning digital currencies, data security, and privacy laws.

Without clear policies, financial institutions and global supply chains remain cautious about large-scale blockchain adoption.

Integrating blockchain into existing workflows is complex. Traditional ERP, CRM, or finance systems may not easily connect with a blockchain platform for business.

This often requires custom app development services or personalized app development consulting to pilot solutions without disrupting daily business operations.

Another business challenge for blockchain adoption lies in governance. Companies must decide between public blockchains like Ethereum, permissioned ones like Hyperledger Fabric, or hybrid models.

Key questions arise:

Without common standards, achieving full supply chain transparency is difficult.

Despite these issues, progress is being made.

Developers are enhancing throughput with Layer 2 solutions and more energy-efficient consensus methods. Industry consortia such as IBM-Maersk TradeLens are working to standardize shared ledgers.

Meanwhile, Blockchain-as-a-Service (BaaS) platforms and SDKs are reducing complexity, making adoption easier for enterprises.

Spending trends confirm this momentum: global investment in blockchain solutions grew from $6.6 billion in 2021 and is projected to reach nearly $19 billion by 2024. (5)

This rapid growth highlights rising confidence and shows that early challenges are steadily being overcome.

The future of blockchain for business is moving beyond crypto and becoming a trusted foundation for secure data sharing, automation, and transparency.

As it blends with other fast-growing technologies like AI and IoT, blockchain is shaping the next wave of digital transformation.

Businesses are finding new ways to use it — from managing intellectual property to strengthening blockchain security and automating supply chains.

Blockchain is transforming business efficiency like never before.

Automating workflows and eliminating middlemen helps companies move faster, cut costs, and boost productivity.

Real-time peer-to-peer transactions replace slow, expensive processes, while smart contracts ensure accuracy and trust without manual checks.

Cross-border payments that once took days now settle in seconds, improving cash flow and reducing operational friction.

With its transparency, speed, and security, blockchain isn’t just an upgrade. It’s the backbone of a smarter, more efficient digital business future.

Ameena is a content writer with a background in International Relations, blending academic insight with SEO-driven writing experience. She has written extensively in the academic space and contributed blog content for various platforms.

Her interests lie in human rights, conflict resolution, and emerging technologies in global policy. Outside of work, she enjoys reading fiction, exploring AI as a hobby, and learning how digital systems shape society.